Luis Alvarez | Digitalvision | Getty Images

Every investor looks to buy low and sell high, which sounds simple enough…until you try to actually put it into practice.

The problem is that it’s seldom obvious when the highs and lows of a particular cycle will happen. Most of the time, that’s apparent only after the fact.

A look at the current environment shows why. On the surface, it looks like it could be time to buy some segments of the market that have taken a beating throughout much of 2022. But perhaps not yet.

With inflation easing slightly, all the major indexes have jumped since bottoming out in mid-October. Meanwhile, Federal Reserve Chair Jerome Powell has signaled that policymakers could increase rates at a slower pace in the months ahead. Therefore, stocks should have room to run going forward.

While that may be the case for some sectors such as health care and energy, some industries are still likely to take on further losses down the road, despite experiencing gains over the last several weeks. Software is one of them.

The software industry enjoyed thunderous peaks during the height of the pandemic-induced lockdowns, only to tumble sharply more recently, with the iShares Expanded Tech-Software Sector ETF (IGV) down more than 30% this year. For a few reasons, however, it’s probably best to take a deep breath and wait a while before snatching up software stocks.

De-risking event

For one, multiple expansions in tech and other interest rate-sensitive industries like software generally occur only when real yields (the difference between nominal yields and inflation) are negative or near zero. Though they have trended down lately, 10-year real yields today remain elevated, hovering around 1.5%.

Second, the business landscape for software sales has become more challenging. The Fed’s tightening cycle has caused many companies to cut spending, primarily through headcount reductions. Notably, that includes the broader tech universe, which spends billions on enterprise software solutions during prosperous times.

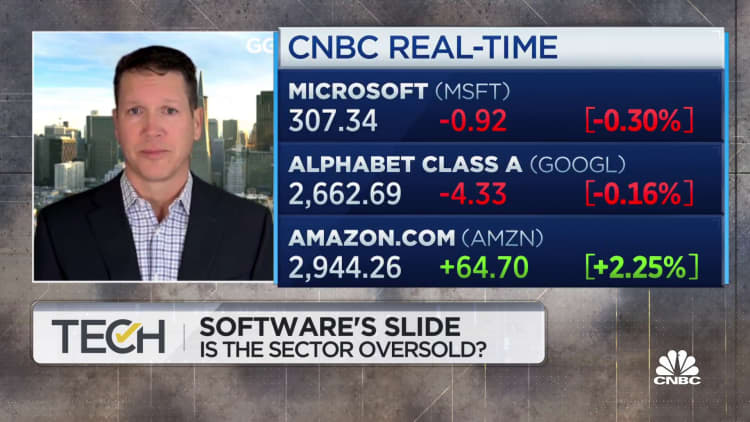

Finally, earnings have been largely disappointed, punctuated by misses in the third quarter by once seemingly invincible mega-stamp names like Amazons (AMZN), Google (GOOG) and Microsoft (MSFT). The fourth-quarter numbers will likely be equally challenging, compelling companies to adjust their 2023 forecasts.

Together, the above forces will create a de-risking event during the late winter or early spring of 2023 that will spark more declines for software firms. That’s when investors should think about buying — not now.

Targets could include the likes of Service Now (NOW), Microsoft and HubSpot (HUBS). All have slumped, lagging significantly behind the performance of the broader market, in the case of Service Now and HubSpot. Yet a coming storm in the software will cause them to decline further.

Clarity in software

Is the latest market momentum actually a so-called dead cat bounce that will soon fizzle out and give way to more sales? Or is it the start of a more substantive rally?

Broadly, it’s hard to know for sure. Markets often give head fakes.

But when it comes to software, the picture is a little clearer. Prices today are likely higher than they will be in February and March.

What’s more, if the Fed tightening continues to gnaw at inflation, real yields could fall even more, providing software stocks a boost from that point forward — setting up an ideal buy-low, sell-high scenario that every investor craves.

— By Andrew Graham, founder and managing partner of Jackson Square Capital